GST on Bank Guarantee given by Directors or Corporates

AUTHOR :Muhammed Mustafa C T

https://taxgtower.blog/brqblog/my_post_view/GST-on-Bank-Guarantee-given-by-Directors-or-Corporates-1-284-423

In corporates, it is quite common to offer personal guarantees to bank by Directors for loans sought by companies or corporate guarantee given by Parent company for loans sought by its subsidiaries. Taxation of GST on such guarantees has been a burning issue as several companies in past has been subjected to GST notices for this.

Now the GST Council in its 52nd meeting held on 07th Oct 2023 has clarified and proposed certain amendments related to Bank Guarantees given by Directors or Corporates to bank against credit limits or loans. The press release states the following rules.

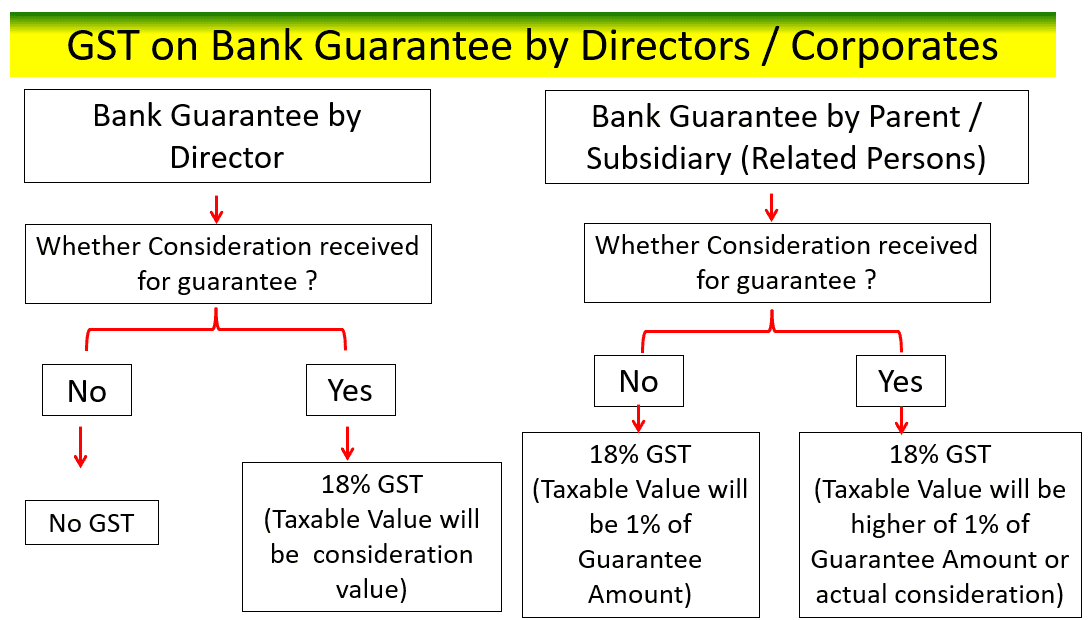

Clarifications regarding taxability of personal guarantee offered by directors to the bank against the credit limits/loans being sanctioned to the company and regarding taxability of corporate guarantee provided for related persons including corporate guarantee provided by holding company to its subsidiary company: The Council has inter alia recommended to:

(a) issue a circular clarifying that when no consideration is paid by the company to the director in any form, directly or indirectly, for providing personal guarantee to the bank/ financial institutes on their behalf, the open market value of the said transaction/ supply

may be treated as zero and hence, no tax to be payable in respect of such supply of services.

(b) to insert sub-rule (2) in Rule 28 of CGST Rules, 2017, to provide for taxable value of supply of corporate guarantee provided between related parties as one per cent of the amount of such guarantee offered, or the actual consideration, whichever is higher.

(c) to clarify through the circular that after the insertion of the said sub-rule, the value of such supply of services of corporate guarantee provided between related parties would be governed by the proposed sub-rule (2) of rule 28 of CGST Rules, 2017, irrespective of whether full ITC is available to the recipient of services or not.

DISCLAIMER:-

(Note: Information compiled above is based on my understanding and review. Any suggestions to improve above information are welcome with folded hands, with appreciation in advance. All readers are requested to form their considered views based on their own study before deciding conclusively in the matter. Team BRQ ASSOCIATES & Author disclaim all liability in respect to actions taken or not taken based on any or all the contents of this article to the fullest extent permitted by law. Do not act or refrain from acting upon this information without seeking professional legal counsel.)

In case if you have any query or require more information please feel free to revert us anytime. Feedbacks are invited at brqgst@gmail.com or contact at 91-96-33-18-18-98.

Disclaimer:

(Note: Information compiled above is based on my understanding and review. Any suggestions to improve above information are welcome with folded hands, with appreciation in advance. All readers are requested to form their considered views based on their own study before deciding conclusively in the matter. Team BRQ ASSOCIATES & Author disclaim all liability in respect to actions taken or not taken based on any or all the contents of this article to the fullest extent permitted by law. Do not act or refrain from acting upon this information without seeking professional legal counsel.)

In case if you have any querys or require more information please feel free to revert us anytime. Feedbacks are invited at brqgst@gmail.com or contact are 9633181898. or via WhatsApp at 9633181898.